Although the Turnbull government recently decided to impose a small Bank Levy on the taxpayer protected five large private banks, it remains a very “banker friendly” government and it has been insistent that there will be no Royal Commission into the role of the private banks in Australia’s monetary and banking system.

Needless to say the large private banks view a Royal Commission into banking with dread and have campaigned incessantly against another one being held.

Another one? You mean there has already been a Royal Commission into the Australian monetary and banking system?

Yes.

In 1937 after the Great Depression a Royal Commission was established in Australia by the Commonwealth government to examine what went wrong.

It is amazing that 10 years after the Great Financial Crisis or Great Recession in 2007/08 we still have not had a serious “root and branch” examination of what went wrong this time.

The bankers and the Treasurer Scott “banker’s buddy”Morrison insist that the reason we should not have another Royal Commission is that there is nothing we need to know. All we need, they claim, are a few more ‘financial sector cops’ on the beat looking for a “few bad apples” and all will be fine.

However, one need only take a quick look at the 1937 Royal Commission report into the Australian banking and monetary system to realise what the bankers and their “support crew” of pet politicians in and out parliament are really worried about.

They know that a new Royal Commission may revisit the fundamental question considered by the commissioners back in 1937:

“What is the proper role of private banks in the Australian monetary system?”

AND come to very different conclusions.

For those that like to read old reports on rainy long weekends here is the full report of the 1937 Royal Commission. 1937 – Royal Commission Full Report

For those that lack the reading time, it is more than enough to read the 7 page dissenting opinion of Commissioner Mr Ben Chifley who did not agree with the conclusions of the other Commissioners in 1937.

Click here for the full 7 page dissent by Mr Ben Chifley. Chifley Dissent

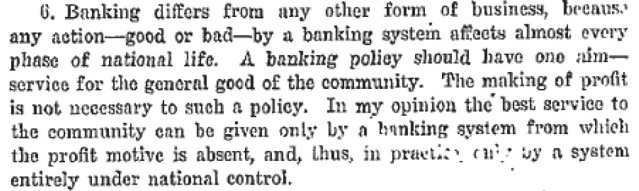

In essence Mr Chifley was of the view that evidence received by the Royal Commission was clear – private trading banks did not act in the general public interest because of their desire to earn profits for their shareholders. He recommended that if a role for private trading banks was to be tolerated they would need to be carefully and closely regulated.

He recommended that those regulations should include, the Commonwealth Bank – at that time still owned by the public – having sufficient powers and operational functions to allow it to provide the public with a banking “public option”. Others might say this was to “keep the bastards honest”.

Hmmmm – isn’t it is odd / disappointing how so many current day ALP members regard Ben Chifley as an absolute labour party legend but ignore his words of wisdom when it comes to the banking and monetary system? One hopes that at least a few of them are now starting to question their ‘faith’ in banking sector neoliberalism and deregulation.

In fact Chifley went so far as to argue in his dissent that the profit motive should be removed altogether by ‘nationalising’ the functions of the private trading banks. Twelve years later as Prime Minister of Australia he sought to pursue that objective but was unsuccessful.

On that point, the Glass Pyramid does not agree with Mr Chifley that “nationalising” the private banks is necessary (or politically possible), instead the Glass Pyramid argues for retaining private banks as private organisations along with their ‘profit motive’ but instead dealing with the ‘problem’ by limiting their operations in a few critical respects. More on that below.

Here are some interesting snippets from Ben Chifley’s dissent

Note: It is best to read the whole dissent as it is very clear and concise and only seven pages long. Chifley Dissent

- In paragraph 2, Mr Chifley makes his position very clear – he doesn’t see a role for private trading banks at all.

- However, as the majority of the Commissioners accepted a continuing role for private trading banks Mr Chifley commented on how such a model should be regulated.

- Here Mr Chifley makes a key point, he notes that if private bankers are going to act in the public interest they will need to be dragged kicking and screaming because the public interest will always be secondary to the profit motive. Anyone who has opened a copy of the Financial Review since budget night will know just how many column inches can be devoted to self interested banker squealing about their ‘profits’.

- The following is a critical point. Mr Chifley notes that banking in our monetary system arrangements differs greatly from EVERY other form of business. This is a critical point because the bank apologists try to pretend that the business of licensed ADI banking is just like any other business and the more the governments keeps out of the way the better. That is nonsense and is discussed in more detail below.

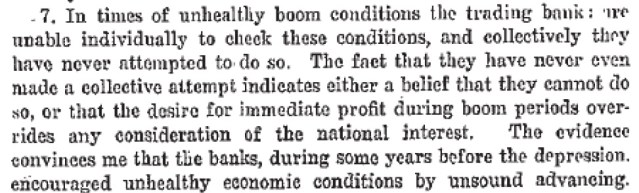

- This paragraph will sound very familiar to anyone with a pulse and sentient during the GFC and during the decades of private bank, debt driven housing booms in Sydney, Melbourne and other capital cities – where at one point Australian banks were even lending to foreign nationals, with dodgy paper work, who wanted to “punt” on Australian residential housing. Mr Chifley points out that banks will lend like maniacs into booms and show no restraint or limits but then vanish and contract leading into a bust and make the bust worse. 80 years later and not a thing has changed. Bankers will keep on dancing until someone ELSE takes away the punch and turns down the music.

- In this paragraph Mr Chifley makes it clear that if we are going to tolerate private trading banks then they need to be closely regulated so that they do not abuse their privileged position as semi-monopolistic public utilities.

Do we need another Royal Commission?

The Great Financial Crisis, the massive levels of household debt, steadily increasing levels of public sector debt and the huge bubbles in Australian house/land prices over the last 20 years make it clear that the issues that the 1937 Royal Commission sought to investigate and address have not gone away.

The role and operation of private banks in our banking and monetary system is dysfunctional and worse, is poorly understood not only by the general public but also by many of the people working within the financial system and public sector.

Our regulators of these private banks, that have grown fat on semi-monopoly profits and have pumped up the asset prices of the wealthy, are timid and conduct much of their important work in secret and via clubby communications. They use the excuse that public confidence might be damaged if the public understood what a massive debt driven / asset price ponzi scheme the private banks are orchestrating and how fragile it is to a strong wind or a limit on taxpayer guaranteed lines of credit.

They prefer to talk about the private banks as ‘stakeholders’ when they are nothing of the sort. Much of the time our regulators at the RBA, APRA and ASIC seem much more concerned about what the banks will think than what is in the public interest.

Back in 1937 Mr Chifley warned the other Royal Commissioners that if private trading banks were to be tolerated as part of the monetary system they would need to be closely regulated. He would be spinning in his grave at what has been going on in recent decades.

From the early 1980s the tight regulation of private trading banks, that was introduced during the decades after the 1937 Royal Commission, was relaxed. The problems resulting from banking and finance sector deregulation are now challenging policy makers in Australia and around the world.

It is essential that another Royal Commission into the banking and monetary system in Australia is held as a matter of urgency and its key term of reference should be to conduct a fundamental review of the issue that Mr Chifley and the other Commissioners concerned themselves with in the wake of the Great Depression.

What role, if any, should private trading banks have in the Australian banking and monetary system.

The Glass Pyramid Position

As noted above the Glass Pyramid’s position is that it is not necessary to nationalise the private trading banks as Mr Chifley suggested in his dissent and which he unsuccessfully attempted to do in 1949.

All that is required is that government credit and currency “Public Money” be completely isolated from the creation of credit by the private banks. In essence this is simply the nationalisation of public money rather than the nationalisation of the private trading banks themselves.

Private banks will remain private but they will lose the public money creation “franchise powers” they have under the current Australian monetary system. Read this for a good explanation of how the “franchise” or Public Private Partnership “PPP” model of public money currently works. Most people simply do not understand that the current model essentially involves giving private trading banks a franchise to create private credit/money that is treated as if it were public sector credit/money.

Ending that “franchise” will address many of the problems that Ben Chifley identified and that have caused the world endless problems since the 1930s and over the last 40 years in particular.

Ending the “franchise” means that when it comes to Australian public money only the Australian Government will have the power to create it and remove it from circulation.

Ending the “franchise” means Private Banks will be allowed to trade in 100% public money and intermediate (bring together) people with savings of 100% public money and people who wish to borrow 100% public money but any private credit they wish to extend must be accounted for exactly the same as it would by any other non-bank organisation or individual.

In other words the private trading banks lose their privileges with regard to the status of the private credit they create.

On the bright side this means:

More freedom for private banks to create and extend their own private credit/money.

More freedom for the government/public sector to create and withdraw from circulation 100% public money.

For more discussion of the ‘franchise’ and why it should end read this

https://pfh007.com/2017/06/07/privatisation-of-public-money-the-first-and-worst-privatisation/

Rather than seeking to control the private trading banks with more regulation, the object of a new Royal Commission into the monetary and banking system would be to end the public money creation “franchise ” that the banks currently enjoy and in doing so set them free.

Most of the “regulation” of the private trading banks was nothing more than an attempt to ensure they did not abuse the “franchise” a privilege that they should never have been given. By ending the franchise the need for tight regulation of the banks will diminish.

It is time we took action to address the fundamental problem that Ben Chifley identified in 1937.

Categories: Macrobusiness

Jeremy Lee. The Plan, how we got here. NWO Australia

LikeLike

COMMONWEALTH OF AUSTRALIA IS A CORPORATION

http://loveforlife.com.au/content/09/09/20/commonwealth-australia-corporation

Is the Commonwealth of Australia, registered as a coorporation in the USA, a legal entity under the Australian Constitution?

Jim Gray made this Freedom of Information request to Department of the Prime Minister and Cabinet

Read on –

https://www.righttoknow.org.au/request/is_the_commonwealth_of_australia

Who owns corporate Australia?

“……………..The reality is that much of Australia’s corporate landscape is owned by faceless people hiding behind big nominee companies that are virtually impossible to research. Not to mention global investment banks, insurance companies and the Commonwealth public servant superannuation scheme. Many companies have directors that are involved in media, banking, and politics, with many ex-politicians coming onto boards when they leave the parliament.

We have seen the close relationships between business and politicians over many governments. And Labor has been able to stay long in government with this accommodation with business interests, ever since Bob Hawke achieved an understanding with a significant group within the dominant corporations of Australia. Big business probably has greater influence at state level, where government can directly facilitate access to prime land and assets that each state controls.

Today in Australia, big business is able to practice what could be called “bully capitalism” where they dictate terms unfairly to smaller businesses. For example rents charged to tenants in large shopping malls are calculated as a percentage of turnover, with systems in place that allow landlords to audit tenant sales, where profit is virtually regulated. Supermarkets in Australia, now that a duopoly exists control over 90% of retail sales, have been able to increase profit margins from 20% in the 1970s to over 50% today.

https://independentaustralia.net/business/business-display/who-owns-corporate-australia,5033

LikeLike

Agency –

1. a business or organization providing a particular service on behalf of another business, person, or group.

Senator George Brandis :-

“It is important to point out that although the ATO is an agency of the Commonwealth it is a different legal personality.”

“Nevertheless, because a constitutional issue had been raised, a notice under section 78B of the Judiciary Act went to the Commonwealth, as well as to the states and territories, asking if the Commonwealth wished to intervene in the proceedings. It is important to point out that although the ATO is an agency of the Commonwealth it is a different legal personality. It nevertheless represents the interests of the Commonwealth in protecting the revenue. It is not automatic that the Commonwealth intervenes in proceedings every time it receives a section 78B notice. Every section 78B notice is assessed according to its own particular facts.”

http://www.openaustralia.org.au/senate/?id=2016-11-28.16.2

The privately owned ATO is effectively a debt collector for the non Constitutional make-believe “Australian Government” IMO. Debt collector laws therefore would apply –

Do I have a contract with you?

https://www.moneysmart.gov.au/managing-your-money/managing-debts/dealing-with-debt-collectors

LikeLike

All Wars Are Bankers’ Wars

April 14 2015 | From: MichaelRivero / Various Sources

A very eloquent and relatively concise video discourse on how and why the title of this piece is so tragically true, followed by a very detailed article for those who wish to read more.

This really is a must see / must read piece to be aware of the real history of banking and warmongering over the last 100 years – along with the how and why such nefarious plans were implemented; and to what ends.

Read on –

http://www.wakeupkiwi.com/false-flag-engineered-wars-1.shtml#BankersWars

https://www.documentarytube.com/videos/all-wars-are-banker-wars

The RBA is a foreign privately owned Central Bank and under section 44 of the Australian Constitution no politician is allowed to sit in parliament while being subject to it.

LikeLiked by 1 person

An interesting read on the Chifley and the banks in 1947

https://www.academia.edu/8119949/Chifley_and_the_Banks_1947_Will_We_Ever_Know_What_Really_Happened

LikeLiked by 1 person

There have been more reports that some of the private trading banks subject to the levy or their minions in the press and parliament have been suggesting that the banks will or should ‘punish’ South Australia by increasing interest rates for borrowers located in South Australia or to limit credit specifically to South Australians.

http://www.sbs.com.au/news/article/2017/06/23/sa-may-pay-levy-opens-pandoras-box

http://www.abc.net.au/news/2017-06-23/sa-bank-tax-could-see-customers-pay-more/8645106

http://www.news.com.au/finance/business/banking/south-australia-defends-desperate-bank-tax/news-story/9fa320324af596944eef5aa9a2f3bb8c

http://www.afr.com/business/banking-and-finance/financial-services/brian-hartzer-says-westpac-rethinking-sa-investment-after-bank-tax-20170623-gwx8bb

Do we really need any better demonstration of the arrogance of these banks?

Threatening to use a “privilege” extended by the public as a weapon against part of the Australian nation?

Unbelievable.

They clearly have lost touch with the reality of what forms the basis of their business model. The indulgence of the Australian public.

What the public gives the public can take away.

As the 1937 Royal Commission discussed at great length. There is no reason to give the credit of one group of private organisations special status and the protection of the state unless it is in interests of the nation to do so. As both the main report and Chifley’s dissent noted the public sector is more than capable of producing in the ordinary course of the business of government all the public money the economy requires at almost zero cost.

When the private banks starting making threats against elected governments they have become far too big for their boots.

Time for a Royal Commission into our private trading banks that looks at one key issue.

“What should be the future role, if any, of private trading banks in the Australian monetary system?”

At the very least the banks need to be put back on a very tight leash.

LikeLiked by 1 person

Thanks for the interesting analysis: Chifley is one of my personal heroes of Aussie history but unfortunately he was undone by his hatred of banks and their power. We would never have become the great industrial nation that we once were if it wasn’t for him… I wonder how he would feel about things like the Rudd guarantee, an extreme moral hazard if there was ever one.

LikeLiked by 2 people

Sean,

Having read his dissent I think it is very clear that it was not hatred but rather an excellent understanding of the inherent dangers in giving private trading bank credit a special status.

I think Chifley erred in his conclusion that the solution lay in nationalising the banks as that turned them AND their staff into implacable foes. Rather he would have been better just removing the special privilege and allowing them to operate purely as intermediaries in public credit and currency.

There is nothing particularly challenging in requiring banks to first acquire the funds they wish to lend, and then lend them on terms consistent which which they were deposited. Non bank investment companies do it all the time. In fact I suspect most people assume this is what banks already do because the banks and their lobbyists like to imply this is all they do do.

There is no difficulty in a government providing a sufficient supply of those funds…public money..to the economy either. As it just requires them taxing a bit less than they spend ….thereby leaving more public money in circulation.

The whole point of the special privilege extended to the private banks was the ‘assumption’ ..I prefer ideological certitude…that private banks would use the privilege to support productive investment that expands the capacity of the Australian economy.

But they don’t. Given the chance and as the record shows they will happily use the privilege to extend credit / betting chips to speculators on the price of existing assets who are making tax effective bets that the banks will extend credit to another speculator and another.

They have abused the privilege and should lose it.

LikeLike

I’m not disagreeing with you about the removal of credit creation powers but Chifley’s idea of nationalisation of the entire banking system was a bridge too far and personally I wouldn’t have supported it; it’s a capitalist society after all.

LikeLiked by 1 person

Sean,

One other point re the Bank Levy that is being imposed by Canberra and now SA.

The private trading banks warrant special treatment because they ARE special.

Especially the Big 5 , who have been able to borrow more cheaply offshore as a result of their effective TBTF status and then use those cheaper funds to dominate the local market.

A levy, much larger than that imposed in the Federal Budget, would do no more than put all of the local banks on a level playing field.

Personally, rather than tax their privilege I would just heavily trim or remove the privilege completely and give it to the public sector (increased expenditure on education, health, training, infrastructure etc) or better still the public (in the form of lower taxes). As I note above the private banks fail to perform the role they are supposed to perform so why not remove the privilege they abuse.

The one sided coverage and broadcast bank sobbing coming from the AFR today is embarrassing. The veiled threats being made towards SA by the bankers and their minions are unpleasant.

Fortunately the general public don’t read the AFR or they would be demanding royal commissions into banking in every state.

LikeLike

PF: Yes, on this point I absolutely agree with you (and Ben Chifley), the social license under which our banks operate demands that they behave to a much higher standard than they presently are. They only operate in Australia because we, the people of Australia, allow them to. We certainly have the right to re-draw the landscape and rules under which they practice.

LikeLiked by 1 person