This is part 3 of the multi-part series “Fixing Oz Banks”. Earlier parts appear below:

- Part 1 – Fixing Oz Banks: Why is “taking deposits” so important to bank “lending”?

- Part 2 – Fixing Oz Banks: Banks ‘leaning’ on the public

Part 1 discusses how private banks use their legal privilege to ‘take deposits’ to create deposits ‘out of thin air’ and demand interest to make them available to the public.

Part 2 discusses how the private bank ‘deposit creation’ for profit model is dependent on and facilitated by the publicly owned Central Bank (RBA)

Part 3 discusses how the relationship between the Central Bank (RBA) and the Private Banks with regard to ‘deposit creation’ should be reversed and the RBA become the exclusive and interest free creator of the deposits required by the public monetary system.

Reversing the ‘deposit creation’ relationship between the Central Bank and the private banks

In simple terms the current relationship between the public Central Bank/RBA and the private banks should be reversed. The RBA should not be bending over backwards and doing everything it can to support the private bank business model, of charging interest for creating deposits ‘out of thin air’. The RBA should instead be creating as many 100% risk free Central Bank deposits as the economy requires and do so at zero cost.

In other words if the economy requires deposits we should stop paying the private banks a stiff fee (interest) to create them ‘out of thin air’ and instead let the public Central Bank /RBA create them ‘out of thin air’ and at zero cost.

Why pay a private bank to do what the publicly owned RBA can do at zero cost?

Once the RBA is in charge of creating 100% of the deposits that the economy requires, the private banks can focus on intermediating the deposits created by the RBA. Ironically, this is what most of the public think they are doing already. So they should not have too much trouble adjusting to the role change.

See Part 1 for an explanation of how banks create deposits ‘out of thin air’ when they record a loan agreement in their accounts.

The purpose of this post is to take a closer look at what the RBA actually does and how it could easily take on the responsibility of creating all of the ‘deposits’ that the Australian economy needs.

The RBA can create deposits out of thin air too!

Parts 1 and Parts 2 of this series spent some time explaining how private banks create deposits ‘out of thin air’. Creating deposits ‘out of thin air’ is not necessarily a bad thing, as all banks do it, but it is important to establish that private banks do it, so the proposal to take away their power to create them is understood.

A lot of private bank enthusiasts, apologists and lobbyists like to pretend that the banks do not create deposits ‘out of thin air’. Invariably they are outraged at the suggestion. Most of the time they insist that banks merely take the deposits of hard working folk and lend them to other hard working folk who are just trying to get ahead. This is misleading and deceptive but their motivation for doing so is obvious. If the public understood that banks create deposits out of thin air (and charge the public to do so) people are likely to take much more interest in and question the rationale for allowing private banks this power.

But rather then be distracted by the bald denials and obfuscations of the private banking squad, the important issue for discussion is who should create deposits ‘out of thin air’ for the purposes of the public monetary system?

The RBA owned by the public or the private banks?

Before we examine why the RBA should be responsible for creating all of the monetary system deposits ‘out of thin air’ rather than the private banks, it is important that we take a look at how the RBA already creates deposits ‘out of thin air’.

RBA deposit creation – just a few accounting entries

The process is quite simple and very similar to how the private banks create deposits ‘out of thin air’.

In short, the RBA buys assets and when it buys an asset it creates a “deposit”.

Dr Asset bought by RBA

Cr Deposit in favour of person selling the asset to the RBA.

Just as private banks create a ‘deposit’ when they buy an asset such as a loan contract.

Dr. Loan contract

Cr. Deposit in favour of person entering loan contract

In both cases the deposits are created ‘out of thin air’ because nothing has actually been deposited and it costs next to nothing to make the required accounting entries.

So what kind of ‘assets’ does the RBA buy?

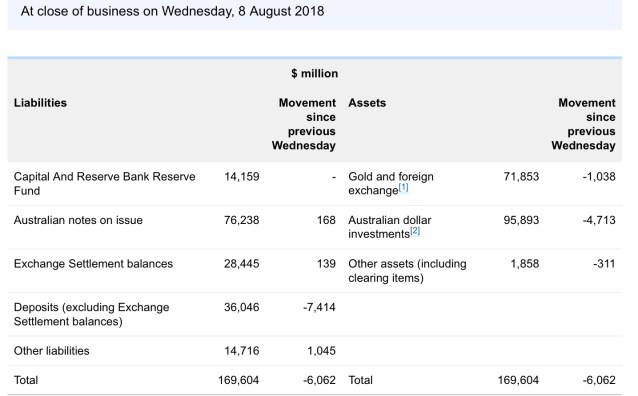

A quick look at the balance sheet of the RBA as at 8 August 2018 shows that its assets currently total $169 billion and consist of three main types of assets:

- Gold and foreign exchange – approx $72 billion

- Other Assets – approx $2 billion

- Australian dollar investments – $96 billion.

On the liabilities side of the balance sheet are four main types of liabilities

- Capital and reserves

- Australian notes on issue – approx $76 billion

- Exchange Settlement balances – approx $28 billion

- Deposits (excluding Exchange settlement) – approx $36 billion

- Other liabilities

Everything on the liabilities side of the balance sheet is a ‘credit’ and everything on the asset side is a ‘debit’.

In addition to the liabilities ($36 billion) that are actually called deposits, the exchange settlement ‘ES’ accounts are also deposit accounts. The ES accounts are the RBA deposit accounts of the private banks / ADI (some ADI share an ADI account). The other deposits are mostly deposits of the Australian governments (especially the commonwealth government)

Every purchase of an asset by the RBA results in a debit entry and a corresponding credit entry.

The RBA purchases of gold are easy to understand. The RBA buys gold and puts in the RBA vault (or some vault elsewhere on the planet) and pays for it by creating a deposit in favour of whoever they bought the gold from. The RBA buys foreign exchange and pays for it by creating a deposit in favour of whoever they bought it from.

The interesting thing about gold is that these purchases usually do involve something being ‘deposited’.

What are the “Australian dollar investment” Assets?

For a detailed breakdown of the Australian dollar investment (assets) click here and check out Note 15 to the Balance Sheet in the 2017 financial statement.

The detail is not particularly important.

What is important is that most of those Australian dollar investment assets are bonds and other securities, in other words ‘bits of paper’ and the purchase of them by the RBA results in deposits being recorded in favour of whoever the RBA bought them from.

The ‘bits of paper’ that the RBA buys are not that much different to the ‘bits of paper’ (e.g. loan contracts) that private banks buy when creating their deposits ‘out of thin air’

The RBA openly acknowledges its ability to create deposits ‘out of thin air’ as follows

“..Liquidity risk is the risk that the RBA will not have the resources required at a particular time to meet its obligations to settle its financial liabilities. As the ultimate source of liquidity in Australian dollars, the RBA can create liquidity in unlimited amounts in Australian dollars at any time. A small component of the RBA’s liabilities is in foreign currencies, namely foreign repurchase agreements…”

So why doesn’t the RBA just directly purchase bonds of the Australian government and in doing so create deposits in the deposit account of the Australian government? Why doesn’t the public central bank lend to the government?

This is interesting and ultimately very revealing about the nature of the operations of Australia’s publicly owned Central Bank the RBA.

The RBA does not buy ‘assets’ direct from the Australian government.

The RBA – owned by the public – may state that it can create unlimited liquidity but it cannot exercise that power when it comes to buying directly Australian dollar investments (bonds) issued by the Australian government.

Clearly the Australian central bank has no reluctance in buying Australian Government financial assets (bonds) – it currently holds quite a few billion of them – but it will not buy any direct from the Australian government. Generally it will only buy them from the private banks.

And we know that the Australian government produces plenty of bonds to buy as the Commonwealth government debt now tops $500 billion, so there is no shortage of potential ‘assets’ for the RBA to acquire.

So what is the problem?

The reason that the RBA will not buy bonds direct from the Australian government directly and in doing so create billions of dollars of deposits is to simply to ensure that the private bank creation of deposits ‘out of thin air’ continues to dominant the Australian monetary system.

It is that simple and blunt.

The RBA does not buy financial assets directly from the Australian government because it is trying to support the domination of the monetary system and the economy by the private banks.

If the publicly owned RBA started started buying interest free ‘bonds’ issued by the Australian government, and paid for them by creating Central Bank deposits in favour of the Australian government, people would quickly realise that there is no need for the private banks to exercise a power to create deposits ‘out of air’ at all.

Needless to say the private banks spend a fortune on political campaigns and strategies to prevent or shutdown and discussion of the possibility of the RBA buying assets direct from the Australian government.

So how does the Commonwealth government obtain deposits for its functions of government if the RBA will not buy any Australian government bonds from the Australian government directly?

Enter our friends the private banks. Surprised?

To reinforce the political idea that the private banks (and not the publicly owned central bank) should be the primary creators of deposits in the Australian monetary system, most of the Australian government bonds are sold to the private banks AND pay interest.

This creates the impression that ‘money’ spent by the Australian government that exceeds tax receipts is coming from ‘someone’ and that is why the Government must pay interest on the ‘money’ it obtains.

It is a deliberately misleading and deceptive process and has a single purpose. To restrict, inhibit and render costly the democratically elected governments access to the fundamental power possessed by the publicly owned central bank……the power to create deposits for the Australian government at near ZERO cost.

The most absurd part of the the “government selling bonds to private banks” scam is that public deposits are actually created by the RBA but in a way that is carefully obscured by a series of accounting entries.

To understand the scam we need to follow the accounting entries for it is the accounting entries that are designed to conceal the scam that is taking place.

The chain of accounting entries that arise from government bonds sales.

The accounting entries below are important because they show how the bond sales triggers a series of accounting entries. Take your time and if you have any questions please ask.

Selling the bond

When the government sells a $100 bond to Bank A its internal accounting entries are:

Debit Deposit at the RBA $100

Credit Bond on issue $100

The internal accounting entries of the RBA are:

Debit ES account of Bank A $100

Credit RBA Government deposit account $100

The internal entries of the Bank A who purchases the bond

Debit Assets (Bond) $100

Credit ES account (reserves) at Central Bank $100

Net result of the above entries

- The Australian government deposit account has gone up by $100

- The ES account at the RBA of the bank has gone down by $100

- The bank owns a government financial asset (Bond) $100 that pays interest

- No deposits have been created by the RBA.

Spending the Australian government deposit

The government now spends the $100 deposit in its Central bank account by paying a pension to a customer of Bank A.

Bank A’s internal accounting entries are as follows

Debit ES account (reserves) at Central Bank $100

Credit Customer deposit account $100

The internal entries of the RBA are:

Debit Government Deposit $100

Credit ES account of Bank A. $100

Net result of the above entries

- Government deposit at the RBA have now dropped by $100 to where it started

- Bank A ES account is gone up $100 to where it started

- Deposit Account of Customer at Bank A has increased by $100

- Bank A still has the Bond asset it bought worth $100

- The effect of the government bond sale has been to provide an effectively risk free AND interest generating financial asset to the private banking system.

In short the process has done nothing more than provide a private bank with something it desperately needs to stop its deposit creation out of thin business model from imploding. A supply of 100% risk free public financial assets.

Government bonds are even better than public notes and coins to a private bank.

Why?

Because the RBA is always happy to buy something as secure as a government financial asset and create central bank deposits in favour of the party selling the asset to the RBA. Just so long as it is not the government that is selling it.

It is completely absurd that the RBA will happily buy the government financial asset from a bank that bought the asset from the government but will not buy it direct from the government.

But then the real purpose of this arrangement is to support and not undermine the privilege of private banks with regard to deposit creation.

If the Australian government wishes to continue to spend more than taxes raise, the sequence of transactions and accounting continue with the result that the bond assets of the private banks continue to rise ALONG with the obligation of the Commonwealth government to pay interest on those bonds or sell the bonds at a discount to their face value.

When the stock of government bonds held by private banks rises into the hundreds and hundreds of billions the cost to the public also continues to rise. To argue, as some do, that the solution is for the government to simply issue more interest bearing bonds (or sell bonds at a discount) to pay the interest on pass bond issues is NO solution.

What if the RBA could buy bonds direct from the Government?

If the RBA was permitted to buy bonds direct from the government the accounting is much simpler.

Selling the bond

First point is that the bond would be sold at face value and would pay no interest. There is no point in having the government pay interest to the publicly owned RBA.

When the government sells a $100 bond to the RBA its internal accounting entries are:

Debit Deposit at the RBA $100

Credit Bond on issue $100

The internal accounting entries of the RBA are:

Debit Australian dollar investments (Bonds) $100

Credit RBA Government deposit account $100

Net result of the above entries

- The RBA assets have gone up by $100 to reflect the purchase of the bond

- The Australian government deposit account has gone up by $100 as the RBA creates the deposit ‘ out of thin air’

- No accounting entries by a private banks because it has no involvement in the transaction

Spending the Australian government deposit

The government now spends the $100 deposit in its Central bank account by paying a pension to a customer of Bank A.

Bank A’s internal accounting entries are as follows

Debit ES account (reserves) at Central Bank $100

Credit Customer deposit account $100

The internal entries of the RBA are:

Debit Government Deposit $100

Credit ES account of Bank A. $100

Net result of the above entries

- Government deposit at the RBA have now dropped by $100 back to where it started

- Bank A ES account has gone up $100

- Deposit Account of Customer at Bank A has increased by $100

- The effect of the government bond sale to the RBA has been to increase both the assets and deposits on the RBA Balance sheet by $100.

- There has been no creation of a deposit ‘out of thin air’ by Bank A as the deposit credit against the customer is matched by an actual increase in reserves at the RBA.

- No interest is paid by the government to the RBA in respect of the Bond

- No interest is paid by the RBA on the extra $100 ES deposit held by Bank A.

- Most likely no interest is paid by Bank A to the Customer on the deposit of $100

Simplest of all?

Even simpler would be to allow the Customer of Bank A to open a deposit account at the Reserve Bank of Australia.

Perhaps along the lines suggesting by:

- Nicholas Gruen in his article in the Saturday Paper

- and by Ross Gittins who endorsed Mr Gruen’s proposal

- The Greens also propose allowing the general public to open RBA deposit accounts but also suggest the RBA start offering loans as well. The Glass Pyramid remains of the view that it is better that the RBA does not get involved in the general business of lending as there are more than enough private, not for profit and other government agencies capable of providing lending services.

Then the accounting entries to record government spending of government deposits at the RBA would be the following:

The internal entries of the RBA are:

Debit Government Deposit $100

Credit ES account of Customer. $100

Pretty simple and no private bank involvement at all.

Which is exactly how it should be for transactions between the Australian Government, the publicly owned central bank and the Australian public.

KEY POINTS

- Just like any other bank, the publicly owned RBA is able to create deposits ‘out of thin air’

- The RBA already buys financial assets created by the Australian government and when it does it creates deposits ‘out of thin air’

- Currently the RBA is not permitted to buy financial assets created by the Australian government directly from the Australian government

- If the RBA were allowed to buy financial assets directly from the Australian government it could do so without any interest or yield obligation on the Australian government. In effect it would be creating new deposits to pay for the financial assets and charging no interest to do so.

- The primary reason that the RBA is not permitted to buy financial assets from the Australian government is to protect the interests of the private banks by

-

- Providing them with a supply of risk free public assets to support their deposit creation “out of thin air” business model by which they charge the public interest to create deposits that the RBA could create at no charge

-

- Provide them with a source of profits in the form of the interest charges and yields on the bonds that the government would not need to pay if the bonds were sold to the RBA directly.

It time for the Reserve Bank of Australia to be authorised to purchase bonds and other financial assets issued by the Australian government.

It is time for the Reserve Bank of Australia to act in the interest of all Australians and not just protect the highly profitable business model of private banks.

Reversing the current relationship between the RBA and the private banks simply involves expanding the already existing power of the RBA to create deposits ‘out of thin’ by buying financial assets directly from the Australian government.

The diagram below summarises how the relationship between the RBA and the private banks with respect to deposit creation must reverse.

Categories: Macrobusiness

Right now I saw an ad on mainstream AU TV asking if cash will disappear. I’ve seen articles where politicians complain about tradies being paid cash(I think you made reference to cash in part 2 and drug dealers whose clients are often well paid bankers).What do your articles do besides clearly illustrating that the minority is gaming the majority(capitalism)? Do the majority really want the disruption needed to change all this? What are the next pragmatic steps? We have the NPP coming which will just be the current system on steroids or a slight opening of the system to the bigger global fish or maybe a few well connected and exclusive “start ups”. The concept of a “fair go” has possibly helped to make AU a reasonably productive economy. What can change at a systemic level so that there will be an efficient flow of units of value(dollars, clam shells, gold ingots whatever the masses will believe has value) to those that are motivated, efficient, helpful and productive?

LikeLike

I lack time at the moment but as per Gen McCarthur – I will return

I find it difficult to comprehend how this discussion can occur on monetary policy and shenanigans without reference to two things

1. The external account and its limitations on Monetary policy (and fiscal policy) – I do recognise that neither does modern economics

2. The role of monetary policy and interest rates in the conservation of the planet. The modern total faith in Negative RAT interest rates presumes that no savings are ever necessary. It therefore presumes a planet that has infinite resources that can be exploited at an ever faster rate forever.

In the words of Gen McKenna – Nuts!

LikeLike

Flawse,

The external account is a constraint because people simply do not give things to others to consume for nothing. If you want some thing you have two choices. Deliver a good or service they want or sell them title to your land, other assets or a claim on your future income.

I do not discuss those issues in this post (unlike a bunch of the other posts) because it is not relevant to the limited point that is being made.

But seeing as you have asked, I would point out that if you are concerned about how manipulating interests rates is a problem and poses a risk for mankind, I share your concern and am of the view that a massive step forward would be a larger role for central bank liabilities that can be created without an interest trailing commission.

Unlike the private bank liabilities which currently constitute the majority of the money supply and the demand for which is manipulated by the manipulation of over night rates by the Central Bank, interest manipulation is much less likely to be a tool of policy under a proposal which involves a much greater role for central bank liabilities.

In fact it might even allow something which you might find most exciting – interest rates set by the market in circumstances where the supply of money is not the result of the decisions of bankers to lend for often completely unproductive purposes.

LikeLike

Joe,

I assume you are referring to this NPP

https://www.rba.gov.au/payments-and-infrastructure/new-payments-platform/

I am not across the detail but considering that the Governor of the RBA insists they have no intention of giving the general public access to deposit accounts at the RBA, I think it is safe to assume that it represents just an updated version of the current model which is dominated by the private banks.

What do the majority want? That is a good question. I suspect most of the majority don’t know enough about the current model to appreciate the nature of the problem and why so many of the things that are making life difficult are at least part linked to the problem.

What can change at a systemic level?

In light of the very real challenges in getting people up to speed on how all the parts connect together the first reform steps must be very modest in scope and very easy to explain.

That is why I have started to focus on the MyRBA deposit account idea.

It is very hard to come up with any decent arguments as to why the general public should not permitted to operate a deposit account at the RBA. After all they are allowed to use central bank liabilities in the form of notes and coins so why not in the form of a deposit account. Especially when the banks not only get to operate deposit accounts at the RBA but they get paid interest as well.

Once MyRBA accounts are available it will be much much easier to start talking about the bigger issue of why we continue to privatise what should be a public monetary system. I have no problem with people offering private monetary systems,e.g. crypto, gift cards and reward points etc (even foreign currency is effectively a private monetary system from the perspective of the locals) but I can see no reason why a public monetary system should be privatised at all.

Cheers!

LikeLike

I’m sympathetic to what’s written here, but it doesn’t engage with the counter-arguments. I don’t think it’s some lame conspiracy. I know people in the central bank and they are not thinking of their role as a simple cover for the banks. It seems you’re arguing for some variant of the Chicago Plan of full reserve banking. That could well be a good idea, but there are plenty of arguments out there that require response arguing that it generates more costs than benefits so I think you need to respond to those concerns.

You’ve described certain aspects of how you want to change the system, but it doesn’t seem to me you’ve then addressed the implications. For instance, the existing system imposes some constraints on governments because interest rates rise as they borrow more. Who decides how much governments can borrow under your system which involves if I’m reading you correctly is analogous to money financed spending. I’m not saying this is necessarily a bad thing, but it opens up plenty of questions which need to be addressed satisfactorily for the model you’re proposing to be convincing.

Also, what are the implications of what you’re proposing for government revenue?

LikeLike

Nicholas,

Thank you for your comment.

It is true I that I have not engaged with counter-arguments directly in this post. While I think my position on many of the likely ones will not be hard to predict, that is still to come along with a plan for staged implementation. If you could identify some more of the counter-arguments beyond the ones in your comment it would be appreciated as I would like to address as many of them as possible.

I am glad you don’t think the current arrangements are a ‘lame conspiracy’ as neither do I. Which is why I have not referred to them as one. There are many ways of describing the current relationship between Central Banks and the banking system, including Public Private Partnership and a Finance Franchise as Hockett and Omarova do.

https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2820176

I think all of them have merit but at core what we are dealing with is an industry that has managed to achieve state support for its private business model and has been very effective at lobbying for that support to be as supportive as possible. That is self interest but it is not a conspiracy. Some of the specific behaviours of the banking industry identified in recent years, including by the current Royal Commission have more than a whiff of a “…a secret plan by a group to do something unlawful or harmful…” but those behaviours are not what I am talking about in my articles.

https://en.wikipedia.org/wiki/Conspiracy_(criminal)

I don’t know people in the RBA but it does not surprise me in the least that they do not see themselves as providing ‘simple cover’ for the banks. I don’t think they provide simple cover. I argue quite clearly that the support given by the publicly owned central bank to the private bank business model is implicit and fundamental.

You argue that is a public / private partnership. A partnership? Bells should be ringing loudly. Imagine a public / private partnership between processed food producers and the health department or education department or one between a manufacturer of weapons and the department of defence?

What would interest me are detailed research papers from the RBA that address head on the key points.

1. Why shouldn’t every Australian (and organisation) have the same access to a risk free deposit account at the RBA as our private banks?

2. Why is the RBA prepared to buy government financial assets from private banks but not directly from the government?

I am not sure what you mean by ‘arguing for some variant of the Chicago Plan’. It might be easier if we deal with what I have said and what your objections are.

Compared to the extensive nature of your proposal and the proposals of the Greens, my suggestions are far more modest.

1. Reverse the relationship between the RBA and the banks from the current relationship where the private banks dominate the creation of deposits in our monetary system.

2. Every Australian would be permitted to open a deposit account at the RBA if they want one

3. The current prohibition (if it is more than a mere convention) on the RBA buying govt bonds or lending to the commonwealth government be lifted.

You said the existing system imposes some constraints on government because interest rates rise as they borrow more. Do interest rates rise? We have watched recent commonwealth governments effortlessly crack $500 billion in debt (with monthly interest payments now exceeding $1 billion dollars) and yet the RBA target rate remains at record lows. Even if the target rate did start to rise how does it constrain government spending? A government may be criticised about the rise in the target rate but it is not constrained…..at least while the AUD holds up.

When comes to constraints on government a far more effective one is the constant and ongoing attention that is paid to inflation (even when the measure of it is tweaked and adjusted to suit). Why would that change? Why would a government be less chastised for rising inflation under a system where the RBA buys government bonds from or lends directly to the government? If anything I would anticipate certain media outlets maintaining a constant and obsessive vigil for the first sniff of milk, bread and grog rising.

I do think that inflation will be something that needs to be watched closely but for the simple reason that that the reduction of interest charges, transaction charges and ‘ticket clipping’ associated with the current model may well mean more room for discretionary allocations of the household budget.

The implications for government revenue? I am not sure what you are alluding to. Government will tax as it currently does however those paying tax will simply be transferring some of the deposits in their RBA deposit account to the government deposit account.

LikeLiked by 1 person

Thanks Mr Pyramid, or can I call you Glass 😉

I’d love to have a discussion with you about it, and you’re welcome to contact me on ngruen at gmail and I’d respect your anonymity to others, but also respect your right to contribute in the valuable way you do without anyone knowing – including me.

The subject is so vast that it’s difficult to cover it here. But when you say you’re just after a simple change, the fact is, it’s not a simple change. Moreover it’s motivated by a basic notion of fairness. All very well, but what we have is a very complex articulated system and you’re proposing fundamental changes to its architecture.

As I was doing the same thing I called my proposal “Central banking for all: a modest proposal for radical reform”. It seems to me your proposal is more radical than mine. I’m proposing utility ‘narrow’ banking run by the central bank with a penumbra of business-as-usual from the existing banks. A lot would change but we’d still be in the same system we have now. Monetary policy would work the same way – albeit more efficiently

In your system I’m not sure what happens. Government debt is monetised. This is regarded as a monster step by the establishment. Adair Turner wrote a whole book shyly suggesting that it could come to that. He clearly thinks it’s a very dangerous business. What are the constraints. You think that governments will avoid inflation – that there are strong disciplines on them to do so.

That’s certainly true now, but that’s after a generation of central bank independence and inflation targeting. One reason governments are paranoid about inflation is that they know that interest rates will rise in that event. And their electorates won’t like that. Before we had central bank independence, inflation gradually rose over the 60s and 70s. There’s the whole literature on the way governments time fiscal and monetary policy to fit in with their electoral priorities.

Anyway, there are plenty of other points to be made. I’m not arguing against you here – I’m drawing attention to what seems to me to be necessary to fill out your argument in order to assess it.

LikeLiked by 2 people

Nicholas,

Apologies for the slow response.

Having the RBA lend to the government directly is a long long way off.

There are kilometres of hysterical AFR op-eds to be written before that would even be considered.

Deposit accounts at the RBA along the lines you have discussed are the only step I am proposing at this point.

So i think that makes me Mr Moderate!

🙂

I think this small step will encourage a much more thoughtful discussion about the appropriate role for a central bank………beyond supporting the operations of private banks.

That is probably the most essential reform.

A proper discussion of what central banks currently do and what they should do. There are many legitimate issues to resolve about the relationship between central banks, democracy and liberty.

At the moment most people have barely the foggiest of what they do and that is a huge problem.

Giving them a MyRBA deposit account might drew more attention to what the RBA does and could do.

Cheers.

LikeLiked by 1 person

The question should not be: “Who (RBA or commercial bank) should be the entitled to charge interest on deposit creation ‘out of nothing'”?

but rather,

“Why should anyone (RBA or commercial bank) be entitled to charge interest on deposit creation ‘out of nothing'”?

The very need for an interest, debt-based money system is what we should all be examining. The “time value of money” argument is circular reasoning, as Colin McKay has clearly previously outlined.

I do agree with your explanation of the “system”, but if the RBA and APRA have done nothing but facilitate, protect and obfuscate the current system and keep it hidden from the general public, then they aren’t ever going to look after the interests of the general public. The system is *designed* this way. The RBA gets its directives from the “above-all-law” BIS in Switzerland, in secret, no less.

“…the powers of financial capitalism had another far-reaching aim, nothing less than to create a world system of financial control in private hands able to dominate the political system of each country and the economy of the world as a whole. This system was to be controlled in a feudalist fashion by the central banks of the world acting in concert, by secret agreements arrived at in frequent private meetings and conferences. The apex of the system was to be the Bank for International Settlements in Basle, Switzerland, a private bank owned and controlled by the world’s central banks which were themselves private corporations. Each central bank, in the hands of men like Montagu Norman of the Bank of England, Benjamin Strong of the New York Federal Reserve Bank, Charles Rist of the Bank of France, and Hjalmar Schacht of the Reichsbank, sought to dominate its government by its ability to control Treasury loans, to manipulate foreign exchanges, to influence the level of economic activity in the country, and to influence cooperative politicians by subsequent economic rewards in the business world…”

– Professor Carroll Quigley, Tragedy and Hope.

I do believe your solution will eventually be implemented, as does Professor Richard Werner.

https://professorwerner.org/shifting-from-central-planning-to-a-decentralised-economy-do-we-need-central-banks/

But together with blockchain technology and the abolition of cash, this will mean complete slavery for humanity.

“I, for one, welcome our central banking overlords.”

LikeLiked by 1 person

Benjamin,

Thank you very much for your thoughtful comments. The issue you raise is important and very real.

I will try and write something on the concerns you raise. Needless to say the reforms I propose would involve some fundamental changes to the operation of the RBA and a number of other reforms along the lines proposed by Professor Werner.

And yes I expect the RBA itself to resist the reforms.

Hopefully I will be able to articulate a process of reform that will be politically possible and avoid the dangers you identify.

Ultimately I am of the view that in a highly centralised banking environment like Australia democratic control of the centre must occur first in order for decentralisation to be possible. Germany wisely avoided centralisation and many of their banks are not for profit so the situation is a bit different there.

I think the path to that involves allowing all members of the public access to deposit accounts (that pay no interest) at the central bank AND abolishing the sale of govt bonds at less than face value (or that pay interest) and sale to anyone other than to the RBA.

LikeLiked by 1 person