Over the last few weeks, the “spooky business” housing market scare campaign by the PM and his “precious” Treasurer has attracted a lot of attention, maybe too much attention, considering its complete lack of substance and the determination of the Sydney property market to demonstrate that “Fear-apalooza” is purely for the 6.30 news and the talking heads.

After a spectacular “Super Saturday” in Sydney yesterday where almost 200 more properties were listed than the same weekend last year to solid clearances and a median price of $1,169,500, now is the time to give praise to the Reserve Bank of Australia “RBA” and the Australian Prudential Regulation Authority “APRA” the real power duo behind the mighty Sydney housing market.

For they shall reign forever …and ever… and ever… and ever.

Why so much praise for a bunch of humble cardigan wearing technocrats?

Because they control the supply and price of credit.. the real determinant of house prices (Sydney and elsewhere). They are the household debt/house price bubble curators and only they shall decide when the bubble shall deflate – with the exception of a collapse of demand for credit (but that is very rare as the ongoing hunger for credit (aka money) in Australia even post GFC demonstrates).

But what you need to remember is that they are extremely reluctant to make even the faintest concession that they are the bubble curators and controllers as that would suggest that fundamental decisions concerning the allocation of resources in the economy are being controlled by unknown and unelected technocrats rather than the elected representatives of the people – the Australian Government. This recent speech by Luci Ellis is a typical example of how the role of the RBA and APRA in driving booms and busts is deprecated.

This is not a unique Australian state of affairs – around the world “independent” central banks and their “credit control” side kicks (like APRA) are making decisions every day as to what industries and groups of individuals will receive buckets loads of the new money created when banks make loans while trying to pretend it is all just the invisible hand allocating capital to its best use.

At the present time large asset owners – such as housing speculators – are receiving lots of sweet loving from both APRA and the RBA. The RBA devotion to the wealth effect is nothing more than the 1980’s “trickle down” theory in new clothing. Let the rich get rich on asset prices and they may pay you to cut their grass, clean their gutters, transact their assets etc.

If you want to understand just how powerful controlling access to credit and the price of credit can be you should read the “Princes of the Yen” by Professor Richard Werner or watch the documentary . In the book and the documentary he explains how the Post WW2 Japanese economy was built on the back of credit pricing and control by monetary authorities and what happens when those making the decisions change their mind on who will get what.

Some of the keener followers of the machinations of RBA and APRA will recall the endless speeches by Gov Glenn and Co in recent years where buckets of ice cold water were poured on the idea of “Macroprudential” in other words – controls on capital – who gets access to credit and when.

They said it would not work, it was unproven, it was fiddling with the invisible, magical and equilibrium seeking hand of the money markets……yadda yadda.

Well as we know that is a bunch of cobblers. What they really meant was “Hush don’t talk about it – we prefer to pretend the magical market pixies are making the decisions”

Of course the decisions on what industries are given access to credit and how much and at what price matters and the RBA and APRA have been making those decisions day in day out over the last 20 years.

While most people focus on the price of credit – the target rate – which is set by the RBA and is itself a powerful driver of the demand for credit due to its influence on mortgage rates, too many overlook the “tools” in the hands of APRA – which determine who gets credit, how much and when.

By comparison, fiddling with the regulations for negative gearing are of little consequence. Even reducing the CGT discount on capital gains is a trivial change when compared to the decisions made by RBA and APRA as to where the torrent of new money – represented by bank lending – will be directed.

As the most commercial and ruthless market in the nation, the Sydney Property Market understands this in spades.

Now that APRA are finally openly fiddling with capital controls (aka Macruprudential) in the form of quiet letters to the banks, directing them to control the rate of growth of credit advanced to investors, the reality of the “capital controls” in the hands of APRA is becoming a bit easier to understand.

Those APRA letters to the banks are not that dissimilar to the “window guidance” given by the BOJ in Japan through the post war period.

Ever wondered how the banks are able to deliver such cheap mortgage rates to home buyers? That depends on APRA allowing the banks to increase their dependence on offshore ZIRP/NIRP lenders in the wholesale market. An absence of unproductive capital inflow controls is a deliberate policy decision.

It also depends on the “weightings” given to mortgage loans on the bank’s books. Give those loans a nice low weighting so that the capital cost of that type of lending is less and guess what happens – banks make more of them and it follows that APRA’s control of those weightings is the real power behind the house price bubble that results.

Harmless?

Well not if you are concerned about our export and import competing businesses being gutted by an exchange rate driven up by all that off shore borrowing by our banks to pump into “low weighted” mortgage operations and therefore house prices.

Not if you consider bidding up the price of existing assets with mountains off shore debt an unproductive allocation of resources.

Not if you consider inducing /forcing people to enter massive 30 year debt contracts for something as basic as shelter is a bad thing.

Look how that graph below for off shore borrowing took off from the mid 1990s and exploded in the mid 2000s and again in 2013 – when house prices exploded yet again – and you can see the very visible hand of APRA and the RBA – hard at work – pumping debt into households and pumping up house prices.

Check out this graph that shows the response of house prices to near ZIRP rates from the RBA. Nothing invisible about that hand in the property market.

Handel’s most glorious praises to the almightly are barely sufficient to acknowledge the power and economic control that has been handed over by the Australian people to APRA and the RBA.

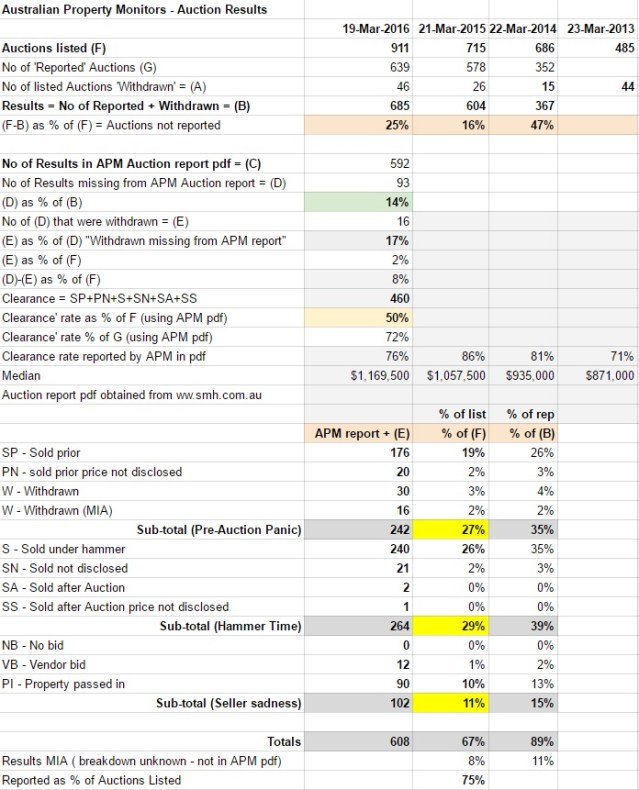

The Sydney Morning Herald and Australian Property Monitors report records that agents reported just 75% of the 911 listed auctions for this weekend which is not great but not dismal either.

Note: In order to encourage agents to help APM collate the most complete stats each Saturday night, the Glass Pyramid is presenting all results as a percentage of the number of Auctions Listed. The reason for this is that agents are more likely to report ‘good results’ sooner and that can tilt the figures when results are presented as a % of what agents have bothered to report on Saturday afternoon.

Anyhow – onto the good stuff!

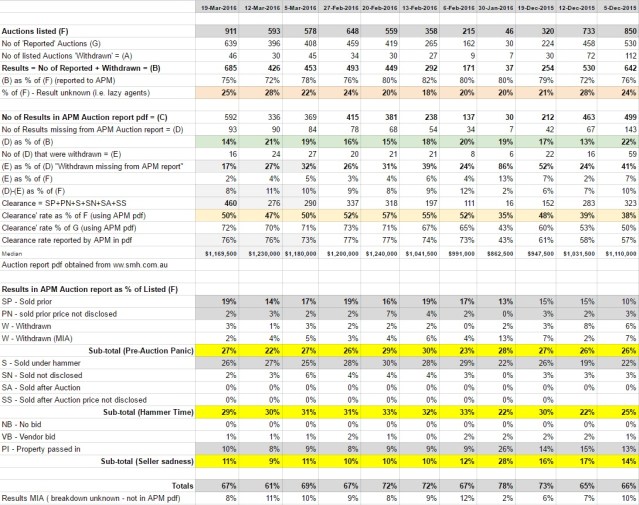

There are two tables this week. The first contains yesterday’s APM fitter and fatter report sliced and diced. The second contains a summary of the last few weeks.

A few comments on yesterday:

- Pre-Action Panic – jumped 5% to 27% of listed auctions with 242 listed auctions not being tested by the hot forge of the market.

- Hammer Time – slipped to 29%

- Seller Sadness – increased to 11% of listed auctions .

Table 1 – Saturday 19 March 2016

Table 2 – Summary of recent results.

Categories: Macrobusiness

Recent Comments