Everyone seems to be agreed that house prices in Australia are high …. very high…. nose bleed high …. international jet set standards high.

Sure there are a bunch of Bernard Salt types roaming the popular press insisting that if people stopped eating squashed tropical fruits and other fripperies they would be able to afford the unaffordable, but most understand that they are being paid as agents provocateur to “stir shit up” with smug prose and distract people from the real issues. Things like how our barbaric relic of a monetary and banking system for instance is ruining our economy.

But in all the column inches devoted to this topic very few discuss how housing prices might return to planet earth WITHOUT crashing the economy.

There seems to be an assumption that prices cannot return from orbit without sending the four horseman into apoplexy.

So whether you are a “crazy Crashnik” who reckons a price purge is unavoidable and good for the soul OR a committed house price bubbler who will vote for anyone who tells you that rising house prices are proof of your virtue and canny thrift and self denial EVERYONE seems to be agreed that if house prices DO fall it will be the end of life as we know it.

There is simple explanation for this miserable state of general agreement.

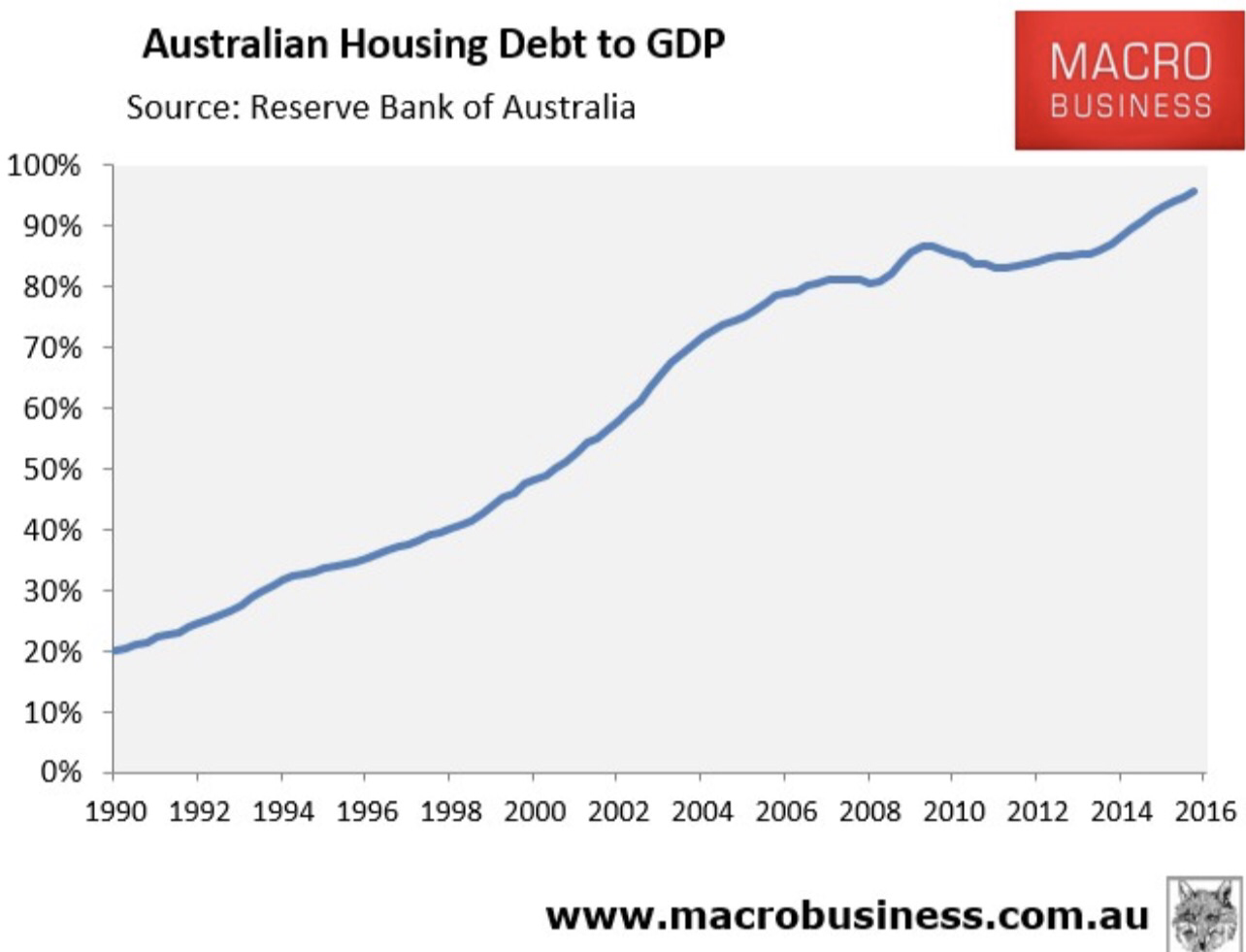

The Australian economy has been thriving on regular and steady increases in the level private debt / household debt for about 20 years. The reason is that the extension of credit by the banks to home buyers amounts to an expansion of the money supply and an expanding money supply makes for a happy economy (especially asset owners).

In other words the banks have been creating hundreds of billions of dollars of new money and spraying it at house prices.

That is why house price inflation has been going through the roof while the CPI type of inflation has remained low. All that new bank created money has been locked up in bank accounts associated with house price speculation. While some trickles out into the wider economy not much.

That weak leakage from the housing market is how RBA and APRA and Scott Morrison rationalise pumping hundreds of billions into the price of housing. It keeps the economy on life support and makes asset owners filthy rich (aka deteriorating inequality). What’s not to like!?

It is a hugely expensive and inefficient method of introducing new money into the economy.

So why did we suddenly think going gaga on household debt was a brilliant idea?

This growing economic dependence on household debt has the been the result of the ideological determination to restrict the use of fiscal policy. If the government doesnt create new money by running a deficit then the reliance on new money created by the private banking sector is even greater and if that mechanism proves inefficient in stimulating real economic activity then ever larger amounts of private debt are required to keep economic activity ticking over.

All that ‘fiscal conservatism’ and balanced budget mania only worked because households were going crazy on debt and the RBA and APRA and guys like Scott Morrison and John Howard were egging the process on with lower rates and tax policy that made speculating on house prices a bonanza.

Is the connection now clear? The switch was all about making private asset owners rich and tying the hands of government.

The sickness and failure of this Australian economic model has become so profound that even as household debt continues to grow to world record levels, Mr Morrison has been forced, despite his bullshit, to run public debt very hard with the outstanding balance now about to crack $500 billion. If he was really worried about the debt he could stop spending but he knows that without the growing debt and the money created by it, the economy would already be in recession.

But this horror story just brings us back to where this post started.

Is there a way out of this mess created by this highly ideological fact free monetary nuttery?

Yes!

But it involves some changes to the preferred method of introducing new money into the economy.

Not big changes but in Australia any change is a big deal.

The first step is to start directly monetising some of the federal deficit. This can be done simply by having the Treasury issue some 0% bonds to the RBA who in return will credit the Treasury Exchange Settlement account.

This means that some of the Federal Deficit (which involves money creation) will now be financed without incurring any interest charge. No interest bill for the kids.

To ensure that this new money does not result in inflation, APRA will place restrictions on the growth of private banking lending to households! The last thing we want is for the private banks to start printing money in the form of out of control lending to households. If they are allowed to do that, inflation may be a risk.

As the supply of “swamp water”- interest bearing new bank credit as public money – slows and is gradually drained and is replaced with fresh water – new publicly created money that is not created with an interest trailing commission attached – the current mess will gradually resolve.

The economy will not be dependent on new private debt to allow interest on earlier private debt to be repaid. Gradually people will pay off their household debts. As people save the new publicly created money and those deposits grow APRA can insist that bankers use an increasing % of deposits deposited at term or specifically nominated for investment to support new lending. In other words become true intermediaries between savers and borrowers.

But will house prices fall?

Yes – without the fire hose of bank created debt being sprayed at them house prices will soften. They are unlikely to collapse but they will go no where for an extended period or slowly decline in nominal terms.

Keep in mind that while housing no longer has a torrent of new bank money directed towards it, the economy will be thriving generally from the reduction of taxes / increased expenditure involved in supplying the new source of interest free public money.

People will be able to pay their mortgages and other people will have incomes to take on mortgages.

But why wont the economy crash?

Because the economy is now no longer dependent on private bank credit creation. Especially credit creation sprayed at house prices. We are now switching to a fresh untainted supply.

A steady supply of new money, that is not created with an interest trailing commission, is being introduced by the government by doing nothing more than the routine tasks of government.

No crazy big government socialism. No grand but dud plans from Canberra.

Even if you hate the current size of government and want to wind back the role of government this approach will still work. Currently the Federal Budget is about $400 billion. If you cut that by 25% to $300 billion you could still add oodles of new interest free money into the economy simply by cutting taxes to produce the required deficit.

As with anything we should start the process slowly to settle all the nervous nellies and hose down the horror stories and fear mongering from the banking industry and then pick up the pace as or when required.

The only thing that is important to keep in mind is that unproductive capital inflows should be restricted to ensure that an inflated exchange rate does not continue to destroy our exports and import competing industries. But this is important regardless of whether action to solve our “public and private ” debt pickle is undertaken.

SUMMARY

We can unwind the stupid policies that made our economy excessively dependent on private bank credit creation.

Doing so will remove the pressure for house prices to rise endlessly as a driver for new private bank credit creation.

Fixing the problem requires only some minor adjustments to how we think about fiscal deficits and how they are financed.

While we don’t have many politicians that have the ability to drive the required debate it will only take a few good ones.

Categories: Macrobusiness

Thanks again for your reply. I would like to know your thoughts on this train of thought..

1. With such a large proportion of commercial banks balance sheets comprising loans on residential property, we can both agree that any fall in the “value” of such property would put the commercial banks/banking system at risk.

2. Should the commercial banks fail, the central bank can step in and buy the bad loans at face value replacing the commercial bank liabilities (“deposits”) with RBA liabilities (electronic, not cash)

3. As those newly purchased “bad loans” will need to be accepted as worthless/near worthless, the RBA may need to revalue another asset already on its balance sheet….that asset being bullion.

4. Obviously this would probably need to happen in a co-ordinated, sudden manner and on a ‘global’ scale.

I guess the suggested solutions in your “summary” in the article above assume that the people in power/control of our financial system want whats best for society etc, but I have a more, shall we say, “conspiratorial” point of view, This stems from the realization that commercial banks are not financial intermediaries like we are taught, but creators of credit ex-nihilo. The need for lies, smoke and mirrors and ‘platypus moments’ tells me something REALLY stinks.

Obviously I will need to take the time and read through your responses and digest them.

LikeLiked by 1 person

Re point 3. Why would the loans need to be accepted as worthless? The RBA will probably just by them at a discount ‘haircut’ and assign any value to them they choose. If the subsequently decide that the loans will never be repaid they could just write them off. I dont think they will be too concerned about what the price of gold might be ‘saying’. It says quite a lot from time to time but is usually ignored. Check out Princes of the Yen on Youtube for what a Central Bank can do when a banking system is stuffed full of bad loans.

LikeLike

I think you might find this interesting as well. It characterises our monetary system as one where the central banks effectively franchised (privatised) the creation of public money to private banks but struggle/ fail to ‘control’ the franchise system in the public interest.

https://papers.ssrn.com/sol3/papers2.cfm?abstract_id=2820176

LikeLiked by 1 person

I don’t understand your statement:

“This means that some of the Federal Deficit (which involves money creation) will now be financed without incurring any interest charge. No interest bill for the kids.”

Isn’t a federal deficit funded by the issuance of bonds (to investors, pension funds etc)? In other words ‘a deficit’ is the difference between government spending and government tax receipts. So this deficit does not involve money creation, as the money used to fund it comes from the savings of the private sector of the economy (which *originally* was created as debt from the process of credit creation)

So, as long as the government does NOT finance its deficit from the act of borrowing directly from commercial banks (which it doesn’t), then the act of running deficit does not involve money creation..

I hope my question is worded clearly for you. Thanks in advance,

LikeLike

Credit Surgeon,

Excellent question.

When a primary dealer buys a bond issued by the AOFM its ES account with the RBA drops by the purchase amount and the Treasury ES account rises.

That is fine and no money creation is involved except that the reduction in the primary dealers ES account will put upward pressure on the interbank rate. To avoid that the RBA will seek to restore the ES balances by buying bonds from the primary dealer.

That steps involves money creation.

In order to maintain a target rate the RBA is forced to buy bonds and it pays with them with created money. Now the purchases may not perfectly match the bonds sales but the point remains that when the overnight rate is targeted govt bond sales must involve money creation by the RBA.

It would be simpler if the AOFM just sold the bonds direct to the RBA but then that would be too transparent and you would not have asked the same question that I asked a few years ago on MB and someone explained to me.

LikeLike

Credit Surgeon,

This is a good read on the topic

http://www.rba.gov.au/mkt-operations/resources/implementation-mp.html

The RBA is focused on maintaining the target rate and that is affected by multiple factors so deficit related bond sales will not necessarily result in a one for one purchase of bonds by the RBA via OMO. So its goal is not to offset specific bond sales. Its target is interest rates not the money supply but hitting that interest rate target affects the money supply.

But the essential point remains that the RBA needs to intervene (and that intervention will affect the money supply) if it wants to maintain an interbank interest target in the face of a government deficit.

LikeLike

Thank you for your reply. I will need some time to read and re-read your answers/link until it makes more sense. In the meantime,

1. could you explain what you meant by ‘MB’

2. If we accept that the RBA can buy bonds and increase the money supply in this way, would that not be reflected in the RBA’s balance sheet? If the total assets on the balance sheet only amount to around 70billion, then surely this method of money creation cannot be thought to be ‘significant’, (when compared to the balance sheets of the commercial “big four”. Again please forgive me if you have answered these already somewhere else/previously.

Thanks

LikeLike

1. http://www.macrobusiness.com.au

2. Good point.

http://www.rba.gov.au/statistics/frequency/stmt-liabilities-assets.html

With only $87B of australian bonds on the balance sheet the RBA does not appear to have bought the bulk of what the AOFM has issued which suggests an alternate explanation for the bulk of circa $400B. Possibly the explanation is the flow of funds from Treasury to the banks. When the bond is bought from the AOFM and the banks ES account is debited and Treasuries credited. The banks ES account is filling up as recipients of treasury’s cheques are presenting them. That may significantly reduce the need for intervention by the RBA. As deficits continue to be incurred the banks holding of IOUs increase but as the money they hand over to treasury comes back to their ES accounts. In addition they receive cheques from Treasury for the interests on the bonds issued which means that a bit of govt expenditure is going to the banks once there are bonds on issue.

As to your original comment – whether bank credit creation can be used to buy government bonds – I dont see why not if it results in a credit ES balance for a bank.

LikeLike