The newspapers are packed to the gills with bad news about COVID-19. In particular the challenges it presents for the Australian economy where our preferred economic model of pumping up house prices, pumping up household debt, pumping up public debt, selling off access to our labour markets and residency, blowing up sacred caves and shipping dirt off to China is coming apart at the seams.

Sadly the core of our economic model is a barely concealed implementation of Trickle-Down economics and after 40 years the fly blown beast is ready for the glue factory.

Fortunately, necessity is the mother of invention and the necessity that is COVID-19 provides us with the perfect opportunity for something new, productive, democratic, equitable and fair.

It is time for Trickle-Up economics served with a fresh crispy MyRBA salad.

Okay but what is Trickle-Down economics?

Wikipedia provides a good account of the history and theory of Trickle-Down economics including the following pithy summary by Samuel Rosenman.

“..The philosophy that had prevailed in Washington since 1921, that the object of government was to provide prosperity for those who lived and worked at the top of the economic pyramid, in the belief that prosperity would trickle down to the bottom of the heap and benefit all…”

In Australia, in recent decades, Trickle-Down economics has been implemented by driving the economy on a rich diet of household debt fed to the “credit worthy” by the private banks.

The start of this Aussie variant of Trickle-Down economics was the deregulation of the private banks in the 1980s (initially by the ALP and Paul Keating and then even more enthusiastically by Howard and Costello in the 1990’s). Deregulation meant that the banks were now largely free to use their privileges, with regard to bank credit creation, to blow a massive bubble in residential asset prices. More wagyu and shiraz waiter!

The theory was that if the “credit worthy” asset owners were made richer by rising asset prices, they would be so excited they would spend some of their new wealth on goods and services and in doing so money would trickle down to the wallets of those delivering the goods and services and all would be well. This “wealth effect” does exist but it is one of the more demented and inequitable approaches to public policy. Naturally by making the banks the centre of economic activity stimulation the “wealth effect” is eagerly endorsed by bank funded “think tanks” and their buddies at the RBA.

Unfortunately, there is a distinctly ponzi element to the Aussie “wealth effect” approach to Trickle-Down economic management, as it requires a steady flow of new people willing to pay even more for housing assets than earlier buyers. But with our governments (Liberal, Nationals and ALP/Green) and the RBA fully on board with the plan it was full steam ahead. The RBA delivered ever lower interest rate manipulations to induce new waves of borrowers to rush down to the nearest bank to load up on more credit so they could jump higher “up the ladder” of housing asset price speculation. Meanwhile the government handed out capital gains tax discounts and ramped up immigration numbers (and foreign speculator access) to maintain plenty of buyer pressure on the lower rungs of the housing ladder.

Having regard to how the Trickle-Down model works it is not difficult see the immense problems that COVID-19 is now presenting for the great Aussie asset price pumping / wealth effect machine.

- The international borders are shut tight so hundreds of thousands of new contestants in the great game that is Aussie housing speculation are not arriving every year and that means less physical demand for housing and less demand for the debt products dished up by our private banks. No surprise that Mr Frydenberg and Mr Morrison are increasingly desperate to get the international borders open as soon as possible. A Ponzi scheme requires a steady stream of fresh players.

- Millions of Australians are out of work and/or dependent on JobKeeper or JobSeeker and those income support payments are hardly a basis for taking on the massive housing loans required to keep pushing housing asset prices up up up.

- The RBA had already driven interest rates close to zero before COVID-19 struck and now the target rate is sitting close to zero at 0.25% ..so there is not much room to goose demand for bank credit with further interest rate manipulations.

- The government is desperately trying to come up with new schemes to throw money and incentives at people to tempt them to jump in and join the fun and have a punt on house prices or to over capitalise their existing house with some tastefully expensive renovations.

No one believes that the Morrison government wants to keep cranking up the level of public debt each month to pay billions and billions in more JobKeeper and JobSeeker payments. Setting new records for public debt is not what conservatives like to brag about.

But what choice do they have? Trying to keep a housing bubble inflated with the international borders shut tight is not going to be easy and if it means cranking up public debt that will take the grandkids decades to pay, well we know what Scott from Marketing will do. Life was not meant to be easy kiddies.

Anyway how is it in the public interest to manufacture interest accruing wealth assets for rich folk (i.e. selling hundreds of billions of dollars worth of government bonds) just to avoid facing the hard fact that the days of the Trickle-Down economic model are coming to an end?

What is Trickle-Up economics?

Trickle-Up economics is simple.

Rather than create money and pump it in at the top of the economy and hope some of it dribbles down, Trickle-Up economics involves pumping it in at the bottom of the economic pyramid and letting it float upwards.

Trickle-Up economics is exactly what we need during a game changing pandemic where traditional patterns of economic activity have collapsed and are likely to have changed permanently. We need every Australian actively engaged in identifying new productive forms of economic activity that work for them and their families and the best way to do that is by having them make real economic decisions every day with money from their own wallets.

If the economy requires “stimulus” let’s stop blowing asset price bubbles with hundreds of billions of dollars of private bank manufactured debt, hoping the “wealth effect” model staggers on a for a bit longer, and start giving some money direct to the general public and let them choose how much they wish to consume, save and invest.

Don’t fall for the myths propagated by the Trickle-Down crew who reckon only wealthy middle class people know how to spend money wisely. Every Australian household is perfectly capable of determining the allocations of money that are in their interests.

Plus the introduction of MyRBA deposit accounts for all Australians at the RBA will make the introduction of Trickle-Up economics very transparent, simple and straight forward. Click here for a Quick Guide to MyRBA https://theglass-pyramid.com/2020/08/15/myrba-the-quick-guide-and-helpful-links/

How would Trickle-Up economics work?

Instead of trying to drive households deeper into debt, by paying too much for houses that are already grossly over priced, and hoping that the resulting expansion of Broad Money due to the expansion of private bank balance sheets somehow dribbles down across the economy, the supply of Broad Money would be increased directly by deposits into the MyRBA accounts of every Australian.

Considering that over the last 20 years the private bank contribution to the expansion of Broad Money was approximately $70 billion dollars per year (and resulted in very little inflation) and we are in the middle of a pandemic that has paralysed the Trickle-Down model, an expansion of Broad Money created and paid quarterly direct to the Australian public of approximately $70 billion per year might be a good starting point.

Assuming that approximately 20 million (80% of the 25 million Australians) would be eligible for Trickle-Up payments, payments of about $875 every quarter into MyRBA accounts would produce an expansion of Broad Money of approximately $70 billion every year or about $17.5 billion per quarter.

Before you panic just remember $70 billion is approximately how much the private banks were expanding Broad Money with their asset price pumping Trickle-Down model EVERY year between 2000 and 2020.

And you wondered how house prices got so high?

And remember that since Scott and Josh decided to vandalise the superannuation scheme by denying low income earners access to genuine income support during the pandemic the withdrawals from super funds over the last 6 months have exceeded $32 billion.

So $17.5 billion per quarter for Trickle-Up economics is quite modest.

But who gets the money as it Trickles-Up from the MyRBA accounts of the general public?

That depends on the choices that you, your friends and family make day in day out. Millions and millions of decisions made by millions of Australians beats a bunch of multi billion dollar Ponzi punts by pollies or bonus hunting bankers.

These are the five broad options for how you spend each Trickle-Up payment of $875

(A) Spend it on goods and services your family needs.

(B) Invest it in some shares, securities or other investment that produces a return that you consider reasonable for the risk associated with the investment.

(C) Allow the government to collect / withhold some of the $875 from you so they can make investments on your behalf (see more about this below)

(D) Do nothing and leave it in your 0% MyRBA account until you need it.

(E) Some or all of the above.

The Trickle Down club simply hate a Trickle-Up approach as their preference is for the current model where the private banks get to create money and give it to people to punt on asset prices or pointy heads in Canberra make choices for you. They find the idea of giving the money to little people and letting them make decisions simply appalling.

Sure a housing bubble is bad but why don’t we just let the government spend it on “infrastructure”?

For some reason, and despite the abundant evidence of recent decades, some folk (lefties, progressives and the mildly woke) romantically cling to the idea that corrupted politicians and the increasingly politicised public service are still capable of making allocations of capital that are in the public interest. In other words we should trust the pollies to pick winners with part or all of each $875 Trickle-Up payment

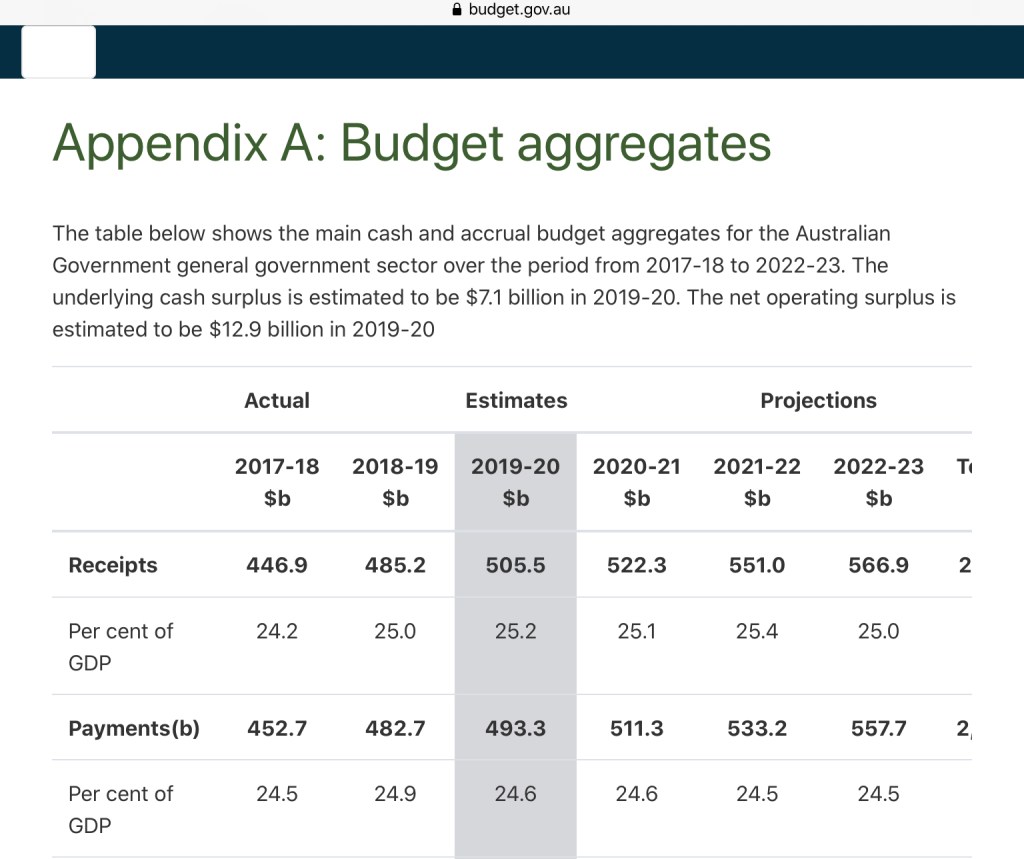

Option C allows for this kind of misty eye romanticism if that is your cup of tea. Option C assumes that you don’t think the government already has more than enough money from taxation to play with. Bear in mind that in the 2019-2020 Josh and ScoMo budgeted to spend $493 billion of the $505 billion they planned to tax you. Are you sure you want them to grab some of your $875 Trick-Up quarterly payment as well?

But let’s assume that you do not believe that the general public are able to identify productive investments and allocate some of their $875 to Option B and that we really need an army of pointy heads in Canberra to work out what is a productive allocation of the public’s Trickle-Up payments.

You would support (Option C) by arguing or campaigning that the government should increase taxes on the public and extract back or withhold some of each of the $875 quarterly payments.

If the government withheld $100 of each $875 payment that would amount to $2 billion per quarter extra for the Canberra Clown circus to spend on productive “infrastructure”. Now of course they might just spray it at electoral rorts so you better watch them closely.

Just remember before you start printing up your campaign posters in Comic Sans

“Make Australia Great Again – Let ScoMo and Josh keep $100 of your $875 and watch them spend it on something worthwhile”

reflect for a moment on some of the more outrageous examples of political pork in recent years.

$100 billion dollar subs ? Sports rorts? Pollie travel expenses?

But where does this Trickle-Up money come from?

It comes from the same place that all money in our monetary system comes from.

Which is the tapping of keys on the computers that make entries into the accounting ledgers of the RBA and the private banks.

Click hear for more information about how billions of dollars of money is currently “ printed” every year in Australia. You might be in for a surprise. https://theglass-pyramid.com/2020/08/09/covid-19-who-are-the-real-money-printers/

The only difference is that the Trickle-Up money that is being created out of thin air is not being sprayed at asset price speculation and is not making a few people very wealthy as the majority scrabble around for crumbs that fall from the table.

Instead Trickle-Up payments are being created and deposited direct into the MyRBA accounts of the 20 million (approx) eligible Australians so they can make their own decisions whether to consume, invest or save.

Surely, giving the general public first use of new money creation is the fairest and most democratic approach to a public monetary system?

It certainly leaves the current broken and gasping asset price pumping unfair Trickle-Down economic model in the dust.

Categories: Macrobusiness

Unless we have one major political party that subscribes to this excellent idea and shouts it from the roof tops in full technicolour its going nowhere.

LikeLiked by 1 person

Steve,

True, and before that is going to happen, a lot more members of the public need a solid understanding of the issue and understand why so many of the problems we are facing result from a fundamentally broken public monetary system.

But things do change.

In less than 30 years we went from gangs throwing gays off cliffs with police looking the other way, to a national plebiscite where even rural electorates voted YES to same sex marriage. And that was just a few years after Gillard and Penny Wong refused to support the idea.

Keep talking about monetary reform and attitudes will change.

After all, asking for deposit accounts at the public owned RBA for all Australians is not asking for much but that simple step will have profound consequences.

LikeLike