NEWS FLASH: The RBA holds – Target rate remains at 2%

Last night the 7.30 report included a story on APRA.

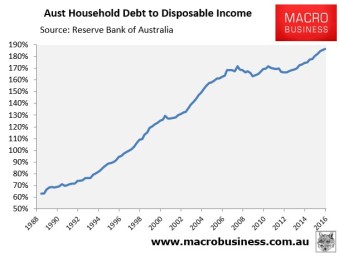

Macrobusiness commented on this story with some excellent graphs charting the massive growth in household debt and the foreign debt that supports it.

Some have suggested that the rise in household debt from from 168% of household disposable income to 186% of household disposable income between 2006 and 2016 is less concerning because interest rates have dropped significantly during that period.

It is not a surprise that if the price of credit is reduced the quantity of credit will rise unless the regulator rations or restricts access or volume – generally or to specific debt consumers.

The result of cutting rates was always going to be a rise in the household debt to disposable income ratio because the price of debt was reduced. More debt (more house buying power) for the same monthly payment etc.

The Bullion Baron graph on the left makes the point by graphing the interest rate cuts by the RBA against Sydney house prices (the price and availability of debt has a powerful impact on house prices)

The Macrobusiness graph below vividly illustrates the mountain of household debt that has accumulated since the late 1990’s.

APRA might have prevented that had it exercised its considerable powers to direct the banks with regard to their lending activities.

But it did not and we know why.

The policy of the RBA and APRA was to drive households deeper into debt; firstly to support the asset price bubble they created in the late 1990s, secondly to allow government to run a “fiscal conservative’ model, thirdly to paper over the GFC cracks and then finally to paper over the sudden end of the mining boom.

The ideological skirt they hid behind to justify their position is the neo-liberal idea that consenting adults are rational and therefore if households want to gorge themselves on massive variable rate mortgages that is their business. This tends to overlook the fact that a pattern of ongoing rate cuts over an extended period will tend to encourage households in the idea that rates only ever go down. Warnings by Gov Glen that rates can also rise do not play well after an extended period where interest rates are driven lower by local and foreign central banks. And that is leaving to one side that ‘rational expectations’ do not make much sense when regulators fiddle with the price of money as they see fit – the market for money is one of the least free on the planet.

They over did it a bit last year (with our friends from China adding some special sauce to the housing pudding) with several Australian housing markets foaming over, so APRA finally exercised some of the powers it had all along. APRA sent some cosy letters to the banks asking them to limit the rate of growth of investor lending to 10% per annum and asking them to ask some tougher questions about borrowers capacity to meet repayments. It is not clear how effective those measures were as the lending to owner occupiers seemed to rise as much as the lending to investors fell. Plus APRA does not seem to have imposed any restrictions on the use of NIPR/ZIRP off shore borrowing by the banks – which if restricted would have put some upward pressure on mortgages rates and rising rates are a very effective way of cooling the overall demand for debt.

Any cooling of the market is likely to be due to the Chinese Government jamming the capital outflow window shut on the fingers of Chinese citizens who have fallen in love with sales brochures for East Coast real estate and deep voiced agents.

The question is what will the RBA (controller of the target rate) and APRA (effective controller of mortgage prices and volume) do now?

They seem a bit shy about pumping the bubble much harder at the moment and so they will probably go slow for a while.

The RBA will probably leave rates on hold today and let APRA tweak at the edges by controlling who the banks lend to and how much.

Who knows what new “suasion” or “directions” will be given on the QT by APRA? Let the investors borrow a bit more? Let owner occupiers have a bit more debt rope?

Perhaps the ATO will redeploy its crack 50 person hit squad away from policing illegal foreign investment or chasing down all those temporary residents who have left the country but have not disposed of their existing property. A softening market will get softer if a bunch of “hot property” hits the market all at the same time.

Perhaps the government will continue to pump up the population with very high levels of migration.

The bubble protection team is a multi-disciplinary team and they move in mysterious ways to keep the housing debt / house price bubble healthy.

But they are playing a dangerous game – if the households of Australia realise that they could be thrown under the bus by RBA/APRA or the government – strapped to their whale loans – as off shore lenders get twitchy and reduce their exposure to the Aussie Housing Bubble or simply because off shore Central Banks engage in some experimental QE for the People experiments and as a result rates start rising – they may exercise some self control the next time the banks run a barrage of cute commercials telling them that debt is as good for them as a glass and half of milk solids mixed with cocoa and sugar.

Categories: Macrobusiness

Recent Comments