Well that did not take long. Only a week after Auction Action warned in “We will make you pay” that the private banks were “crunching credit” to teach us a lesson about who is running/wrecking the joint and would make the nation beg, Treasurer Frydenberg is already waving the white flag! Surrender is not a good look Josh when there are better alternatives. And yes, the auctions lacked action again this week.

No surprise that the Bankers Bugle (aka the Australian Financial Review) was first with the news.

The article included a quote by Mr Frydenberg.

“I would encourage the banks when it comes to lending, in particular for small business, make sure you get the balance right, keep the books open and don’t lose sight of the broader public good.

We all know the royal commission has brought into focus the issues of responsible lending and examples of misconduct. While both issues are important, I do see them to some extent as separate, with different responses required.”

What on earth does Josh mean when he uses expressions like “get the balance right”, “keep the books open” and “don’t lose sight of the broader public good”?

Since when have private profit making companies needed to be asked to keep working or required to factor in something as nebulous as the “broader public good”. Next Josh will be asking the bank CEOs for free hugs and pats for puppies. A very strange and pleading tone from the Treasurer of the Australian government.

According to “mainstream” fiction the role of banks is simple. Banks accepts deposits of money from savers and then lend this money responsibly to borrowers, and that means borrowers who are willing to pay interest on what they borrow and appear likely to repay the loan principal as well (and if that promise is not enough the bank may accept as security a mortgage of assets owned by the borrower).

If banks are performing this ‘role’ as a financial intermediary why do they need to contemplate what the “broader public good” might be? Surely if they just lend as much savers money, as they can, to good borrowers, they are doing the right thing by the savers, the borrowers and the nation?

The reason of course is clear.

The role of the private banks in the Australian monetary system is NOTHING like the fairy stories that we are told about their “role” and the statements by Mr Frydenberg, as he pleads and waves the white flag of surrender, confirm this. Does Mr Frydenberg really believe that banks have lots of ‘savers’ money but are refusing to lend it? And if they don’t how could they lend what they do not have?

In the Australian monetary system what should be a purely public power in respect of the creation of public money has been largely privatised and for the most part the decisions on when public money (to be precise, banks create an effective substitute for real public money) is created, are made by the private banks and this happens when they decide who they will lend to and for what purposes. If the banks don’t lend they are not creating new public money and because people are continuing to repay old loans (which reverses the process) the money supply can start shrinking very quickly.

So it is entirely natural that when the effective controllers of the public money power (aka the Banks) go on strike and effectively stop creating money, which is what a “credit crunch” is, the Treasurer of the Australian Government is forced to beg them to return to work. Not that the Banker’s Bugle or the bankers themselves would ever describe a bankers “credit crunch” in such terms.

Why are the bankers currently on strike?

Because they dont like being criticised by the Banking Royal Commission and are on strike until Mr Frydenberg offers them better protection for their past and future lending (money creation) decisions. Considering that the government is already guaranteeing their depositors and the RBA stands ready to buy their loan books if no one else will, they are becoming incredibly demanding with an overwhelming sense of entitlement.

It is time to call their bluff.

So what is the alternative?

The alternative is obvious.

Why on earth are we allowing the private banks to control the exercise of what should be an entirely public power? The creation of public money.

It is time to start unwinding the privatisation of the public power in respect of public money. Reform needs to start RIGHT NOW.

The following should be the key objectives for Mr Frydenberg :

- Reduce the domination by private banks of our public money system. Less banker private bank liabilities “Banker Pseudo Fiat” as public money and more central bank liabilities as public money.

- Provide Australian families and other first home buyers with a low cost (very low interest if any interest at all) public backed borrowing option when it comes to buying their first home.

- Break the bankers ability to hold the national economy to ransom with a “credit crunch” or Bankers Strike.

The initial steps in the reform process are as follows:

- MyRBA accounts for all Australians – Expand the role of central bank liabilities in the Australian monetary system and reduce the role of private bank liabilities by allowing all Australians (and non-banks) to operate a simple deposit account at the Reserve Bank of Australia. As Australians transfer some of their deposits from accounts at private banks to the RBA the balances of the private banks ESA deposit accounts at the RBA (yes the banks are already allowed to operate deposit accounts at the RBA) will start to fall. To create additional central bank liabilities the RBA can start buying some government securities from the private banks by crediting the banks ESA accounts. This will allow for more deposits in the banks ESA deposit accounts at the RBA to be transferred to MyRBA deposit accounts of individuals and non-banks. Once central bank liabilities as public money have been created the private banks cannot destroy them or hold them hostage. For more details click here

- Low interest lending to First Home Buyers. Establish a government home lending service (this service should not be provided by the RBA) with a mandate to provide low interest first mortgage lending to first home buyers and owner occupiers – especially owner occupier buyers of new housing. This will help break the banker’s ability to strike in the form of a “credit crunch” for home buyers. The capital to establish this new lending service will be provided by the government and will be raised by issuing government securities that are sold direct to the RBA. This will ensure that any interest paid on the bonds is received by the publicly owned RBA. The government may appoint existing credit unions, building societies and not for profit banks to assist in the delivery of the program. The construction of additional public housing may also receive finance as part of this program. The objective of the program will be to achieve healthy levels of residential tenancy vacancies across the nation. 4-5% may be the initial target having regard to the effectiveness of vacancy levels of circa that size in reducing rents and house prices in Perth and Darwin.

- Private Banks to focus on business lending – Without the ‘distraction’ of generic lending to owner occupiers and first home owners the banks can concentrate on rebuilding their skills in lending to business which Mr Frydenberg actually has some grounds for criticising. Investors (aka speculators) in residential housing can continue to borrow for their property speculations from the private banks but over time it is likely that as healthy levels of housing supply reduce the returns from the current housing asset price casino, investment in more productive ‘business’ activities may receive more attention.

Below is the full series of Glass Pyramid posts on reforming Australian Banks.

- RBA Watch – Money Money Money!

- Bank Royal Commission: The wisdom of Ben Chifley in 1937

- Part 1 – Fixing Oz Banks: Why is “taking deposits” so important to bank “lending”?

- Part 2 – Fixing Oz Banks: Banks ‘leaning’ on the public

- Part 3 – The best way to create deposits? – The RBA v the private banks

- Part 4 – One small step at a time

- Part 5 – What happens next?….more small steps

- Part 6 – Making a difference?…a response to Joe

- Part 7 – What should be the role of the RBA?

- 100% safety for your savings? The RBA will not allow it.

But now lets get to the Auction Action stats for this week.

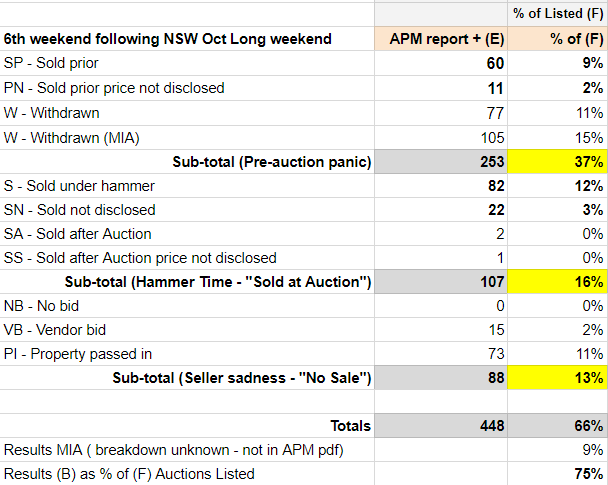

Table 1: Hammer Time

Table 1 shows the totals for each auction result category in the APM pdf reported by Domain this week. Hammer time is the percentage of the listed auctions that were sold under hammer or shortly afterwards.

Sold under Hammer was a woeful 12% this week with a high level of auctions being withdrawn (26%).

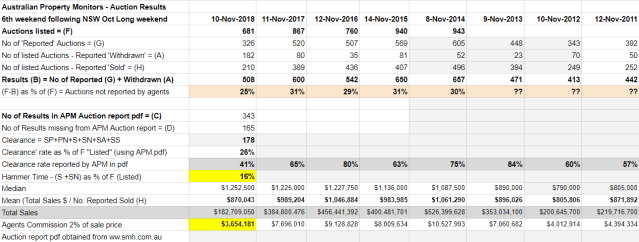

Table 2 – Year on Year comparisons

Table 2 compares this weekend (the 6th weekend after the October long weekend) with the same weekend in the previous 8 years.

It is good to see that the Agents are reporting the results with only 25% of the listed auctions not reported. But the bad news is that what they were reporting was not good. A clearance rate of 26% of the listed auctions and only 41% of the reported auctions. The value of the total sales was only $182M compared to the $380M – $525M sold on the same weekend in the previous 4 years.

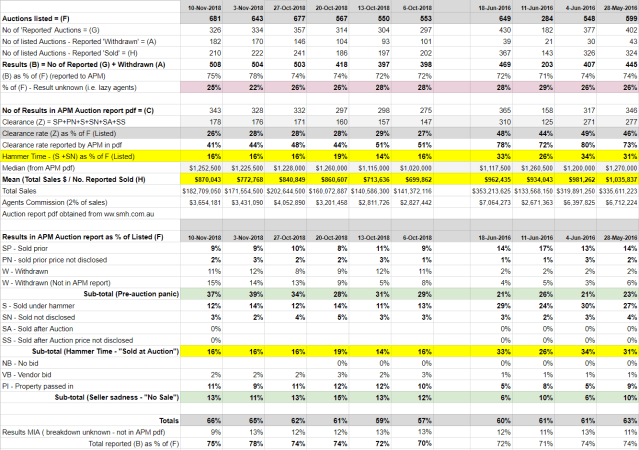

Table 3 – Summary

Table 3 is a summary of recent weeks of auction action. Some 2016 figures are included to remind us all what credit taps turned to full can do!

If there are rainbows hiding in this data they are very small and hard to see.

Categories: Macrobusiness

Recent Comments